Social Security, An Actuarial Analysis of the Benefit Gap and Implicit Debt

Written by:

Ahmad Al-Dmour

Economic Affairs Researcher

Legitimate questions are being raised regarding the ability of Jordan’s social security system to maintain financial efficiency and sustainability over the coming decades, these concerns are grounded in genuine actuarial, demographic, and economic considerations rather than merely theoretical apprehensions, the sustainability of any pension system depends on a delicate equilibrium between collected contributions, realized investment returns, and disbursed insurance benefits, This article provides answers and clarifications to these critical questions.

First: The Existence of an Actuarial Imbalance Between Contributions and Benefits

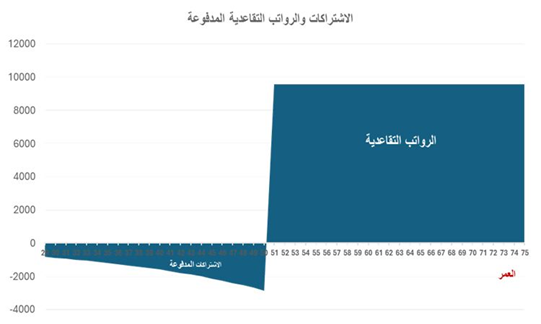

This imbalance stems from the structural design under which the Jordanian pension funds operate within the social security system. The system follows a Defined Benefit (DB) model, whereby the retirement pension is determined according to statutory formulas linked to the insured wage and the number of contribution years, rather than being based on the actual accumulated balance of each contributor.

Such a structure generates an actuarial gap when the present value of expected retirement benefits exceeds the present value of paid contributions.

In cases of early retirement in particular, this gap widens significantly due to the following factors:

● A reduction in the actual contribution period.

● An extension of the pension payment period over a longer time horizon.

● An increased financial burden arising from survivors’ benefits.

From a purely financial perspective, achieving individual actuarial balance between total contributions paid and expected benefits would require exceptionally high investment returns, in some cases exceeding 12% annually. These required returns may rise even further when the insurable wage increases shortly before retirement. Such rates are difficult to achieve on a sustainable basis without assuming elevated levels of investment risk. This approach contradicts the fundamental nature of pension funds, which are expected to prioritize prudence, stability, & long term sustainability.

Second and Most Critically: The Impact of Demographic Changes

Any social insurance system that relies, even partially, on a “Pay As You Go” (PAYG) financing mechanism depends fundamentally on what is known as the dependency ratio that is, the number of active contributors relative to each retiree, reference to demographic change here is intended to clarify the transitional phase from a period of relative stability to one of structural imbalance, a shift that may have gone largely unnoticed in previous years.

Historically, Jordan’s social security system benefited from a youthful demographic structure, whereby the number of contributors significantly exceeded the number of retirees. This favorable ratio enabled the system to absorb actuarial gaps temporarily.

However, the gradual demographic transformation characterized by rising life expectancy, slower labor force growth, and an increase in the number of retirees at a faster pace than contributors has led to a decline in the dependency ratio; consequently, actuarial gaps have shifted from being manageable imbalances to an accumulated obligation, economically referred to as the pension system’s implicit debt.

Third: Incentive Problems and Behavioral Distortions

Pension system studies indicate that certain distortions arise when the insurable wage increases significantly in the final years preceding retirement, or when individuals retire at the minimum legally permissible age.

Although such practices are legally compliant, they may weaken intergenerational equity and increase pressure on the system, as the calculated benefits do not always proportionately reflect the actual lifetime contributions accumulated throughout the individual’s working career.

Fourth: The International Context

The challenges facing Jordan’s social security system are not unique. Pension systems in many countries have encountered similar structural pressures; for example, several European states have been compelled to gradually raise the retirement age, revise benefit calculation formulas, and partially transition toward schemes more closely linked to actual contributions in order to contain long-term liabilities.

Moreover, international institutions such as the World Bank and the Organization for Economic Co-operation and Development (OECD) consistently emphasize in their periodic reports that early and gradual reform is socially less costly than delayed and abrupt adjustment measures.

Analytical Conclusion

The core issue does not necessarily lie in the existence of an immediate deficit, but rather in a long-term trajectory characterized by the accumulation of obligations that may exceed projected resources if well-designed structural reforms are not undertaken; accordingly, ensuring system sustainability requires aligning the statutory retirement age with demographic developments, put plainly, recalibrating retirement age parameters.

Equally important is enhancing investment efficiency without exceeding prudent risk thresholds, while linking benefits more closely to the totality of actual lifetime contributions.

The discourse surrounding social security must therefore move beyond narratives of reassurance or alarmism toward one grounded in actuarial analysis and quantitative transparency. The sustainability of the system is not merely a financial concern; it is fundamentally a matter of intergenerational equity and long-term economic and social stability.